Why Execution Quality Matters: Latency, Slippage, and Fill Rates

In professional trading, execution quality is not a luxury—it is the single most important variable separating consistent profitability from unpredictable results. When milliseconds determine outcomes and fractional spreads compound into meaningful performance differences, the integrity of your broker’s infrastructure can make or break your strategy. Knight Markets was built on one principle: transparency and precision must always come before marketing slogans. Understanding latency, slippage, and fill rates will show why execution quality is the ultimate measure of trust.

Defining Execution Quality

Execution quality refers to the accuracy and speed with which a trading order is processed from initiation to fill. In an institutional context, it encompasses three measurable dimensions: latency, slippage, and fill ratio. Each reflects how faithfully your broker or prime-of-prime executes your intended trade under live market conditions.

High execution quality means the system delivers consistent fills at the requested price with minimal delay. Low execution quality often signals hidden friction: slow routing, internal dealing desk interference, or shallow liquidity pools that cannot handle real-world volume.

Latency Explained

Latency is the time between when a trader sends an order and when it reaches the liquidity provider. It is measured in milliseconds, but even tiny differences can distort strategy outcomes. For high-frequency or algorithmic systems that rely on microsecond precision, latency is the enemy of performance.

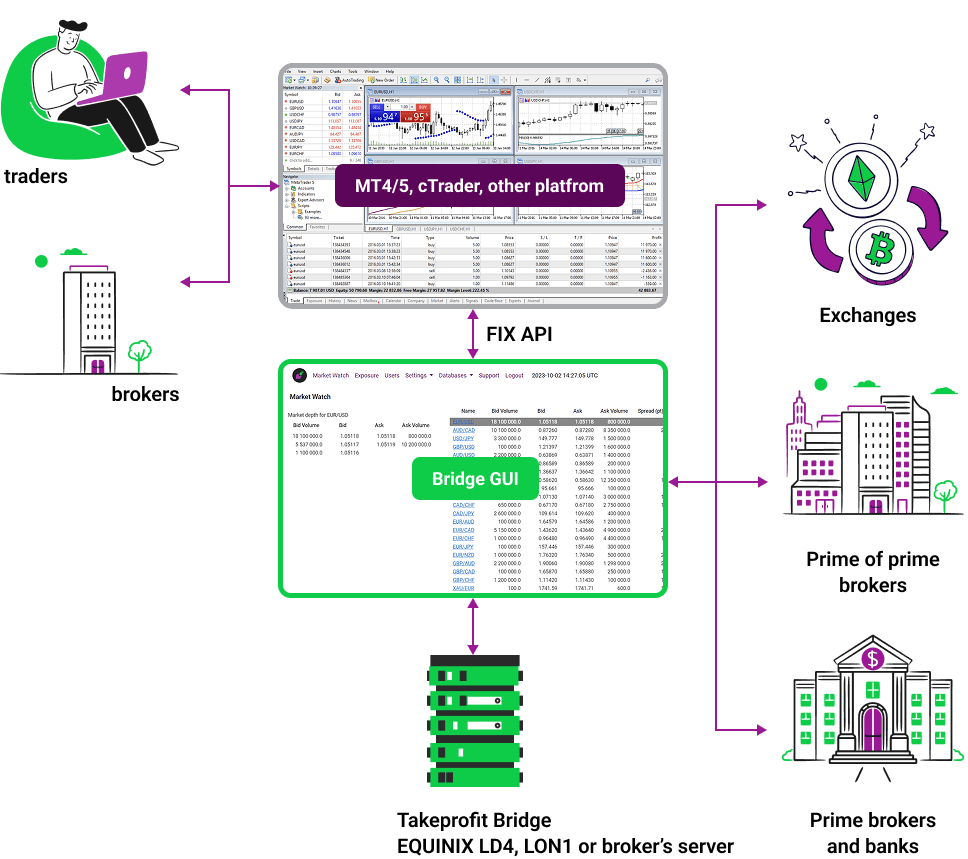

The sources of latency are typically structural. Poorly placed servers, overburdened aggregation engines, and inefficient routing logic all contribute to delayed execution. True institutional providers minimize latency through co-location with major liquidity hubs, optimized network paths, and direct FIX API connections.

At Knight Markets, latency is treated as an engineering problem, not a marketing point. Orders are routed through strategically located data centers that maintain persistent connections with Tier-1 liquidity providers, ensuring real-time order transmission with negligible lag.

Slippage and Its Impact

Slippage occurs when an order is executed at a price different from the one requested. In volatile markets, some slippage is natural, but chronic, asymmetric slippage often indicates deeper issues. For traders, the difference between expected and actual fill prices accumulates into significant profit erosion over thousands of trades.

There are two primary types of slippage: positive and negative. Positive slippage occurs when a trade is filled at a better price, while negative slippage costs the trader. A reputable prime-of-prime provider allows both to occur naturally as a reflection of genuine market conditions. By contrast, brokers operating on internal B-Book models often suppress positive slippage while passing all negative slippage through to clients.

Transparency in slippage data separates true A-Book providers from synthetic ones. Knight Markets routinely provides transaction cost analysis reports that quantify execution variance so trading groups can verify integrity.

Fill Rates and Reliability

The fill rate measures the percentage of orders executed successfully at the requested price. A low fill rate suggests thin liquidity or a broker manipulating fills to manage internal risk. A consistently high fill rate, by contrast, reflects deep market access and stable aggregation logic.

Professional trading systems require predictable fill ratios to backtest and forecast results accurately. Without reliable fills, model variance increases and strategy calibration breaks down.

Knight Markets maintains exceptional fill ratios by aggregating liquidity across more than sixty Tier-1 providers. Orders are routed dynamically to the best available venue in real time, ensuring competitive fills even during high volatility. This multi-provider aggregation also reduces re-quotes—another hidden cost that plagues retail-level brokers.

The Hidden Costs of Poor Execution

Every millisecond of latency and every pip of slippage is a silent tax on performance. For systematic traders executing thousands of transactions per day, that tax compounds rapidly. Poor execution turns otherwise profitable strategies into breakeven operations.

Brokers that internalize flow or manipulate execution may appear to offer tight spreads but hide their costs in slippage and re-quotes. The illusion of low cost vanishes once true performance metrics are calculated.

To evaluate whether your provider is helping or hurting your performance, compare average fill speed, positive versus negative slippage ratios, and order rejection rates. If these metrics are unavailable, transparency is already an issue.

Comparing A-Book and B-Book Execution

The difference between A-Book and B-Book models becomes most apparent when analyzing execution quality. In an A-Book setup, trades are passed through to external liquidity providers where market depth determines the fill. In a B-Book model, the broker effectively controls both sides of the transaction.

That control creates room for manipulation: artificial delays, widened spreads, and selective execution that favors the broker’s book over the client’s performance. For professionals, such conditions are intolerable.

If you missed our breakdown of this structural difference, read “A-Book vs B-Book: How Broker Models Impact Your Edge.”

Technology as the Foundation of Speed

Superior execution begins with infrastructure. Institutional providers invest heavily in data center architecture, cross-connects, and routing algorithms to achieve sub-millisecond performance. Retail brokers, on the other hand, often prioritize marketing over engineering.

Knight Markets’ infrastructure was designed for one purpose: to remove friction between trader intent and market execution. FIX API connectivity allows automated systems to transmit orders directly, while our smart-routing algorithms distribute order flow intelligently across liquidity sources based on pricing depth and current market load.

For a closer look at the technology stack supporting this execution model, see “How Technology Architecture Supports Trading Edge.”

Transaction Cost Analysis (TCA)

For institutions, verifying execution quality requires data, not promises. Transaction Cost Analysis provides the quantitative foundation for assessing latency, slippage, and fill integrity. A transparent provider will deliver granular reports showing order timestamps, quote sources, and execution pathways.

Regular TCA reviews allow trading groups to detect hidden inefficiencies and optimize their strategies accordingly. At Knight Markets, these reports are not optional—they are part of our commitment to open reporting.

The Relationship Between Volume and Execution Quality

Volume drives liquidity, and liquidity drives execution quality. When brokers internalize client flow, they remove volume from the open market, reducing depth and widening spreads for everyone. A true prime-of-prime amplifies liquidity by routing all orders externally, contributing to the health of the overall market.

This is why Knight Markets’ A-Book model scales so effectively: the more clients trade, the deeper and more efficient the aggregated liquidity pool becomes.

Market Volatility and Resilience

High-volatility conditions reveal a broker’s true capabilities. Many platforms perform well during calm periods but collapse under stress—spreads widen, orders fail, and execution speed degrades. Institutional infrastructure must be engineered for resilience under stress.

Knight Markets tests its routing systems under extreme conditions to ensure consistency even during liquidity crunches. Our multi-venue aggregation model ensures that if one liquidity provider withdraws during turbulence, others continue to quote, maintaining continuity.

Human Oversight and Automated Precision

While most of the execution process is automated, human oversight remains essential. Monitoring order flow, latency metrics, and liquidity performance allows continuous optimization. Knight Markets employs hybrid monitoring—advanced automation supported by experienced risk and technology teams—to ensure execution quality remains consistent at scale.

How to Measure Your Own Execution Quality

Professional traders can and should audit their own execution data. By comparing timestamped order requests against actual fill confirmations, latency and slippage can be quantified directly. If your platform does not provide raw execution logs, request them. Transparency is the hallmark of an institutional-grade provider.

Building Trust Through Measurable Performance

Execution quality is the clearest reflection of a broker’s integrity. Marketing promises can be copied; latency data cannot. The numbers tell the truth. That is why Knight Markets invests in infrastructure first and advertising second. For trading groups managing serious capital, performance and transparency are not negotiable—they are the baseline.

The Institutional Standard

Over the next decade, the gap between retail and institutional execution quality will continue to widen. Regulation, technology, and competition will push serious traders toward transparent, A-Book environments with verifiable data. Those who remain in opaque systems will face widening friction costs and diminishing control.

Knight Markets remains committed to setting the institutional standard through deep liquidity access, full transparency, and a technology-first approach.

Conclusion

Execution quality defines everything that follows in professional trading. Latency, slippage, and fill rates are not technical jargon—they are the operational DNA of profitability. Choosing a broker that understands and prioritizes these metrics is the most strategic decision a trading group can make.

At Knight Markets, we measure our success by the precision with which we deliver yours.